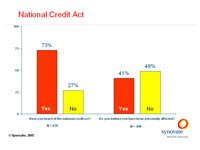

Interestingly, only 44% stated that their banks had communicated with them about the NCA.

The highest proportion of those who stated that they had been affected by the NCA were males, as well as respondents in the 20 – 24 year age group. “This is very possibly due to the high amount of credit application that takes place during this lifestage and the fact that in South Africa males are still the primary ‘financiers' for their families,” states Debbie Amm, Client Services Director at Synovate.

Most respondents had applied for vehicle and asset finance, a homeloan or personal/study loan. Very few had applied for store cards or accounts.

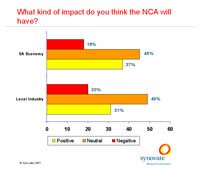

A third of those interviewed believe that the NCA will have a positive effect on the local industry, while 37% believe that the act is good for the overall South African economy. “The fact that there is a substantial degree of public support for the law is very positive,” states Amm. “The NCA is aimed at alleviating over-indebtedness in our country and there has been a lot of negativity around increased administration and restraining of industries that rely on the granting of credit. It is great to see that South Africans back the act.”

When asked about how the credit application process had changed, 34% who had applied for credit described the process as ‘very simple'. “This is very possibly due the fact that, when applying for vehicle finance or even a homeloan, very often the Finance and Insurance department/mortgage originator will take care of your application and you have very little to do until your signature is required at the end of the process,” continues Amm.

At the other end of the spectrum, 25% described the process as ‘difficult' or ‘very difficult', the majority of which were Black and Coloured respondents.

Of those who had recently applied for credit, 68% had their credit approved. “It is hard to tell whether this is a result of the NCA,” states Amm. “It is very possible that credit applications would yield the same success ratio purely due to the level of the applicant's income or a bad credit history.”

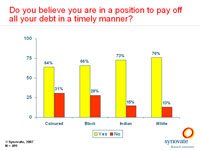

Are South Africans in Debt?

Almost a quarter of the respondents believe that they are not in a position to pay off all their debts on time. This is especially pronounced in the Coloured and Black population groups and the younger age groups. “It is natural that younger age groups will have more debt than older age groups. Those between 18 and 34 are typically in the first phase of independence. This means a great deal of initial expense as they start to establish themselves by paying off student loans, buying a car and finding a place to live,” explains Amm.

Interestingly, despite the NCA, a relatively large proportion (28%) of respondents stated that they had recently been contacted by a South African credit provider who offered them credit they had not applied for, either via post (53%) or telephone calls (44%). An overwhelming 91% did not take up the offer of credit – a very positive response from a public that has been criticised for having too much debt.