International climate commitments

The Paris Agreement is an international global climate change agreement that aims to limit global temperature increases by substantially reducing global GHG emissions. Having signed the Paris Agreement in 2016, South Africa has undertaken to reach a goal of net-zero GHG emissions by 2050. To meet this target, South Africa made various climate commitments that were presented to the United Nations Framework Convention on Climate Change at the 2021 UN Climate Change Conference.

Carbon tax regime and budget speech effects

To this end, South Africa has introduced the Carbon Tax Act no. 15 of 2019 (Carbon Tax Act) which aims to curtail GHG emissions by levying a tax on every ton of carbon dioxide equivalent of GHG emissions by those taxpayers who conduct listed activities within South Africa. The tax is determined by combining the taxpayer’s fuel combustion, industrial processes and fugitive emissions, expressed as their carbon dioxide equivalent (CO₂e).

The carbon tax rate was introduced to South Africa at R120/tCO2e with an annual increase of the Consumer Price Index (CPI) rate plus 2% during the first phase, now sitting at R144/tCO₂e as per the Budget Speech. The Carbon Tax Act does however make provision for certain deductions and allowances which reduce the carbon tax liability to an effective tax rate of between R7 and R58/tCO₂e. These include a basic 60% allowance to which all carbon taxpayers are entitled, as well as various other conditional allowances such as fugitive and process emission, trade exposure, performance, a carbon offset, and a carbon budget allowance.

These will likely be reviewed and decreased during the second phase, which commences at the start of 2026. In this regard, Treasury has stated that toachieve the Paris climate goals, the basic tax-free allowance will gradually be reduced from 2026 to 2030, and the threshold for the maximum trade exposure allowance will be adjusted from 30 to 50 percent from the beginning of 2023, making it harder to utilise the full trade exposure alliance. On a positive note, however, to encourage investments in carbon offset projects, the carbon offset allowance will likely be increased by fivepercent in the second phase.

A more concerning change to the carbon tax regime is Treasury’s intention to penalise emissions exceeding the taxpayer’s mandatory carbon budget. This mandatory carbon budgeting system will be effective from the beginning of 2023. At this time, the carbon budget allowance of five percent will fall away and will be replaced with a higher carbon tax rate of R640/tCO₂e to be levied on all GHG emissions exceeding the taxpayer’s carbon budget. This change, to be contained in the Climate Change Bill once promulgated, will likely result in an exceptionally high carbon tax liability for companies who are unable to remain within their carbon budgets. This includes, for example, those taxpayers in the iron and steel industries, who are already likely to face reduced competitiveness on their exports due to overseas border taxes for carbon-intensive goods.

Carbon tax has been implemented in a phased manner, with the first phase initially set to end on 31 December 2022. The Budget Speech however saw the announcement that this first phase will be extended to 31 December 2025. This is beneficial as it enables taxpayers to continue utilising the available allowance and deductions in their current form. It was explained by Godongwana that the ’transitional support measures’ afforded to South African companies during this first phase, such as ‘significant tax-free allowances’ and ‘revenue-recycling measures’ will still be available during this extended first phase.

Furthermore, while an electricity producer will calculate its carbon tax liability in the same manner as other carbon tax liable entities, electricity producers are, and have always been, eligible for an additional benefit. This benefit allows them to subtract from their carbon tax liability the amounts of any renewable energy premium and the amounts of any environmental levy, leaving them with a net-zero carbon tax liability if they are eligible for both deductions. It was explained in the Budget Speech however that while Treasury has committed to extending electricity price neutrality until 31 December 2025, the electricity-related deductions will be limited to the carbon tax liability of fuel combustion emissions and will not be offset against the total carbon tax liability. The ‘energy-efficiency savings tax incentive’ will also be extended to the end of the first phase.

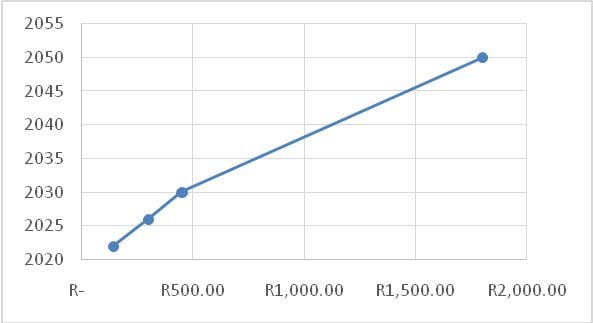

A concerning aspect of the Budget Speech’s carbon tax announcement is Treasury’s proposal to progressively increase the carbon price every year by at least $1 to reach $20/tCO₂e by 2026. This means that in four years, assuming an exchange rate of R15 to the US dollar, the carbon price will sit at about R300/tCO₂e, almost double today’s rate. Even more problematic is government’s intention to continuously increase the carbon price more rapidly each year so that it is $30 (R450)/tCO₂e by 2030 and $120 (R1,800)/tCO₂e beyond 2050, as is demonstrated in the graph below.

Rightly so, Godongwanasaid in the 2022 Budget Speech that “we urge all our companies that have not already done so to develop plans to progressively reduce their emissions over the next 10 years, otherwise they will face these steep taxes.”

The 2022 Budget Speech has made it very clear that Government is serious about decreasing its GHG emissions to meet South Africa’s international climate commitments and recognises carbon tax as the main mechanism by which to do so. As a result, it is apparent that Treasury intends to intensify our carbon tax regime by imposing higher rates of carbon tax to drive compliance with the mandatory carbon budget regime, increase in carbon price and a reduction in certain incentives.